Request a Demo

Request a Demo

Summary:

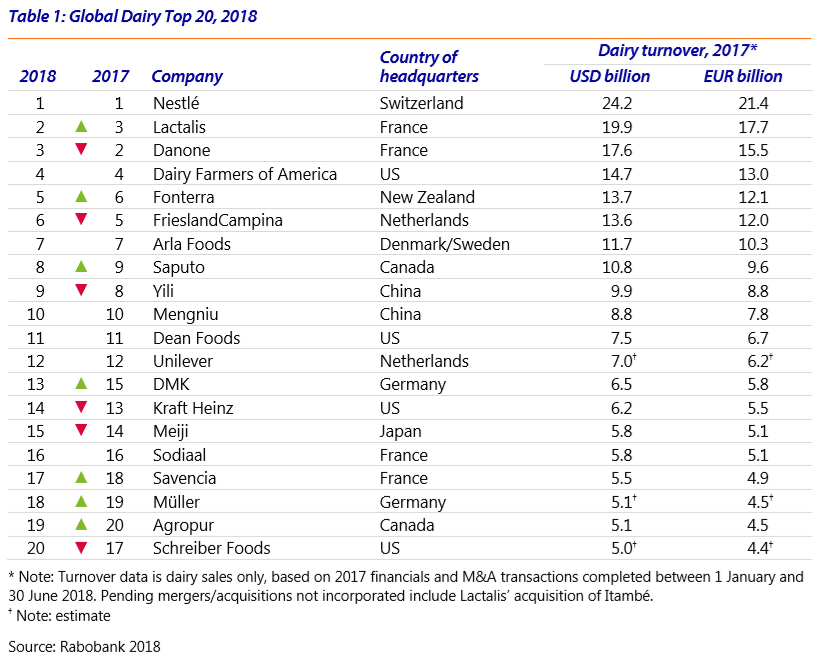

The latest annual Rabobank survey of the world’s largest dairy companies highlights the giants of one of the world’s most valuable food sectors. Dairy price recovery in 2017 has positively affected the combined turnover of the top 20 companies, which, in 2017, was up 7.2% on the year in US dollar terms and 5.1% in euro terms.

M&A is on the rise

Merger-and-acquisition (M&A) activity in the dairy sector grew in 2017, fuelled – as in other sectors – by the availability of cheap capital. However, unlike other food & agribusiness sectors, the megadeals which did occur – Danone/WhiteWave and Saputo/Murray Goulburn – had limited impact on rankings within the Global Dairy Top 20. As a result, there are no new entrants in the list for the second consecutive year, with the USD 5bn threshold apparently difficult to break through.

M&A activity in the dairy sector is accelerating. There were 127 deals in the dairy complex in 2017, compared to 81 transactions in 2016. As of mid-2018, the number of dairy deals stands at 62, with nearly half occurring in Europe. In 2017, the transaction value fell below the prior year, due to fewer large deals. Moreover, some of the largest deals in the dairy sector occurred outside of the Global Dairy Top 20, as illustrated by Mexico-based Grupo Lala’s acquisition of Brazil’s Vigor. Over the next few decades, Rabobank expects the dairy market to grow by at least 30% in volume and value, as a result of population growth, income growth, and urbanization. Both organic growth and acquisitions will be growth drivers. Nevertheless, Rabobank forsees some challenges in achieving this milestone.

Cooperatives still dominate... but are also challenged

The dairy sector trails other sectors in terms of industry consolidation through large-scale acquisitions. That is not to say that M&A doesn't occur in the dairy sector – it just means that dairy acquisitions tend to be limited in size and financial impact. In contrast to other F&A sectors, the dairy industry is dominated by large farmer-owned cooperatives. In fact, cooperatives occupy the fourth through seventh positions of the Global Dairy Top 20. Together, the four largest dairy cooperatives accounted for nearly USD 54bn in turnover in 2017, more than double the annual turnover of Nestle, which occupies the top position in the top 20.

Dairy cooperatives operate in a challenging economic environment. Dairy farmers struggle with creating ‘farmholder’ vs. ‘shareholder’ value. This is allocating capital/investing in their farm operation, rather than growing their cooperative’s shareholder value through M&A or plant expansions. The expectations of many farmer-cooperative members to receive the maximum milk price has left the cooperative with limited funds to support future growth. Also, dairy cooperatives face a constant battle to find the right and/or innovative structure to help access outside capital, with the high-profile failure of Murray Gouburn leading cooperative boards to be more risk-averse. While cooperative mergers are less risky and need less capital, these are often smaller, more complicated, and local – often within the country borders.

The dairy cooperatives that comprise the Global Dairy Top 20 reflect many corporate mergers over the past several decades, which have mostly occurred within a country’s border. But acquisitions by dairy cooperatives of privately-held companies or publicly-traded companies’ purchases of cooperatives have more often across borders. Publicly-traded Saputo acquired US-based Alto Dairy cooperative in 2008. A decade later, Saputo purchased Australian dairy cooperative Murray Goulburn, making Saputo the largest dairy processor in Australia. In 2008, Dairy Farmers cooperative in Australia became a part of National Foods, then owned by Japan’s Kirin, Lactalis acquired Swedish cooperative Skaenemejerier in 2012. Canada-based dairy cooperative Agropur purchased US-based, family-held Davisco Foods in 2014, after previous acquisitions of family-held cheese companies Trega Foods (Wiscosin) and Green Meadow Foods (Iowa). Earlier this year, publicly-traded Brazilian Adecoago purchased Argentine dairy cooperative Sancor.

China considers global growth opportunities

Chinese companies need to address the integration of non-Chinese management as they consider growth opportunities around the globe. Increased collaboration between Chinese and non-Chinese companies in China has the potential to create a pipeline of global management talent. At the same time, there is an opportunity for non-China-based companies to increase their presence and participation in the Chinese market and dairy sector.

Local or global... or both?

Historically, the dairy industry was very local. That is, milk production, processing, and consumption occurred locally. This was particularly true in markets dominated by fluid milk consumption. However, economies of scale in milk production and the conversion of milk into longer shelf-life products like butter, cheese, and dry dairy ingredients has required many dairy companies to be more globally-oriented. In the case of Europe and the US, dairy companies cannot lose sight of their large, domestic markets, which may demand more local attributes such as sustainability and traceability. Furthermore, environmental constraints are likely to limit production growth in some countries and/or regions. As a result, these dairy sectors are likely to develop new local sourcing and processing models, requiring new capital and offering new investment opportunities that are less influenced by the interplay with traditional milk-producing regions.

The disruptors are here!

Moves such as Danone’s decision to but WhiteWave and increase its focus on plant-based alternatives, or the emergence of biotech developments (e.g. the suggestion that, in the future, it will be possible to culture dairy proteins rather than extract them from milk) has sparked an interest in innovation. Rabobank sees an increased amount of ‘disruption’-based M&A deals, either defensive or opportunistic. By nature these deals are often small and involve start-ups, but they are growing in volume.

2017 review: the moves in detail

Dairy price recovery in 2017 positively impacted the combined turnover of the Global Dairy Top 20companies, which was up 7.2% on the year in US dollar terms and 5.1% in euro terms. For the second consecutive year, there were no new entrants to the list, with the USD 5bn threshold difficult to achieve due to a scarcity of large acquisitions or mergers.

However, while the names have remained the same, the order shifted in 2017. The world’s largest food&beverage company, Switzerland’s Nestle, reigns supreme on the list, but the gap between number one and number two has narrowed. French Lactalis swapped places with compatriot Danone and moved into second place, boosted by its acquisitions of US yoghurt business Stonyfield and Siggi’s. Danone slipped to the third spot, after advertising Stonyfield following the acquisition of WhiteWave, reducing its stake in Yakult, and selling its holdings in the AI Safi Danone joint venture in Saudi Arabia. In India, Danone has decided to focus on nutrition products, and it has sold its dairy plant to a local player.

New Zealand’s Fonterra moves into fifth place, slightly ahead of Dutch-based FrieslandCampina, which fell to sixth place. Arla Foods remains in the seven slot, despite a buyout of the joint venture with SanCor and a new joint venture with Indofood. Saputo leapfrogs Yili and moves into eighth place, helped by the acquisition of Australia’s Murray Goulburn, along with two acquisitions in the US and Canada.

To achieve their ambition to be leading global companies, the Chinese giants Yili and Mengniu will need to make international acquisitions. Yili remains the largest Chinese/Asian player in the Global Dairy Top 20, while Mengniu maintained its number-ten position. The two Chinese players showed a combined sales growth of 9% YOP in 2017 in US dollar terms, following a more difficult 2016.

German DMK moves up two places, as a result of its restructuring and repositioning at the expense of US-based Karft Heinz and Japan’s Meiji.

Disclaimer:

This report was first published on rabobank.com

We provide full-scale global food market entry services (including product registration, ingredient review, regulatory consultation, customized training, market research, branding strategy). Please contact us to discuss how we can help you by

We provide full-scale global food market entry services (including product registration, ingredient review, regulatory consultation, customized training, market research, branding strategy). Please contact us to discuss how we can help you by