Request a Demo

Request a Demo

Infant formula regulation in China over the last decade has been inextricably linked and shaped by the vagaries of market dynamics, protectionist policies and technical capacity disparities between China and its international competitors. While the sheer scale of the market makes it a mouthwatering prospect for international and domestic dairy enterprise and investors, the volume and value of the market belies the true risk inherent in China infant formula sector market entry. Risk and rewards are equally great, and the road to success in China’s infant formula sector is littered with the carcasses of less savvy investors or enterprise unable to buffer the disruptive influence of constant regulatory change over the last several years. Accepting that risk is inevitable are there any metrics or information we can use to guide safer investment? Is this even possible, given that companies like Bellamy’s (with multimillion dollar consultancy budgets) have failed in China due to the destabilizing influence of new regulations. Are there any signs of what is likely to happen over the next several months and in the coming years? Here are our 4 predictions:

1. More preferential policies for domestic infant formula products

According to Nielsen data [1] the market share of domestic infant formula surged from 25% in 2008 to 43.7% in 2018, and its growth rate in maternal stores (the major infant formula sales channel) channel reached 25.4% in 2018, which is much higher than that of imported infant formula (10.1%). Chinese consumers now have much more confidence in domestic products and the data shows the CAGR of domestic infant formula consumers on JD platform has jumped to 35%.

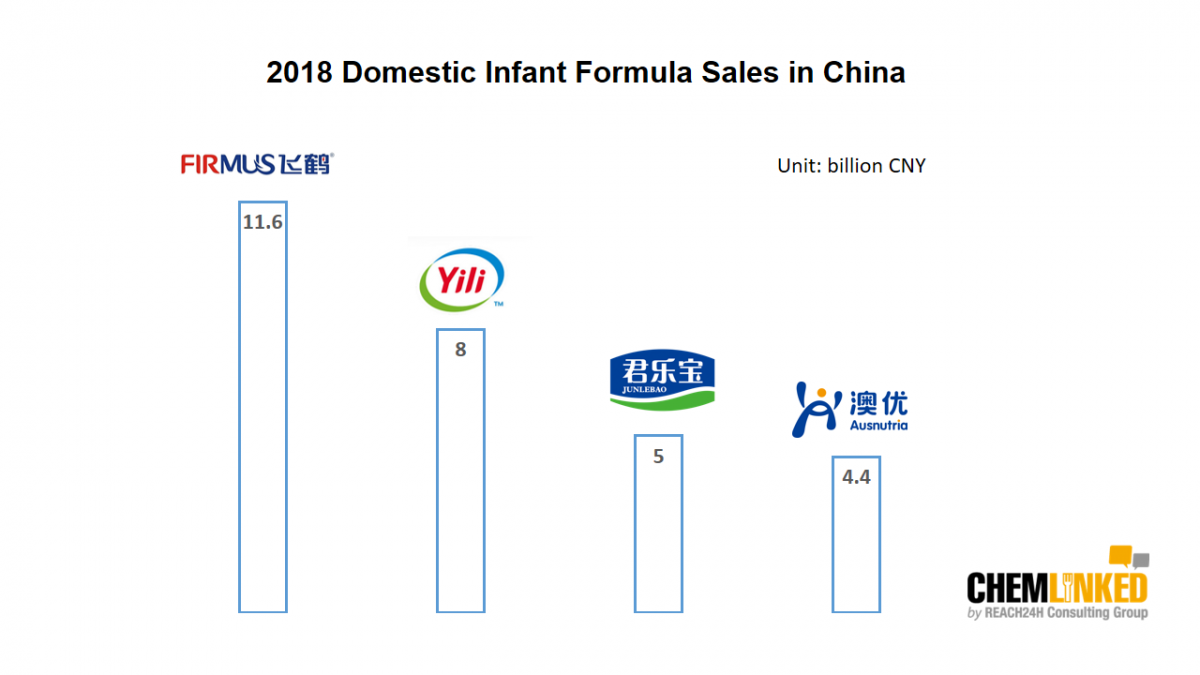

Undoubtedly the positive market performance of domestic infant formula products is closely associated with the government’ support and preferential policies. In June 2014, former CFDA, MOF, MIIT and NDRC (National Development and Reform Commission) jointly issued the Work Program on Promoting Infant Formula Enterprises’ Merger and Restructuring [2], which aims to foster the development of 3-5 largescale infant formula enterprises whose annual sales exceed 5 billion Yuan by 2018. Obviously this target has already been realized by Firmus, Yili and Junlebao, and Firmus even became the first domestic infant formula brand whose sales value hit 10 billion Yuan in China. Milk source and raw material quality is another key foundation stone of the dairy sector that the Chinese government aims to improve. In June 2018 the State Council unveiled the dairy industry revitalization roadmap, prioritizing the establishment of premium milk source bases. Later in announcement No.1 [3] issued by the State Council this year, the development of dairy bases and improvement of infant formula product were mentioned again. All of these actions showcase China’s determination to revitalize its domestic infant formula industry and overhaul its whole industrial chain. In the next few years, infant formula revitalization will still be the theme of government’s work, and the competent authorities are expected to release more preferential policies, subsidies and incentive scheme to promote continued progress in China’s domestic sector.

Milk source and raw material quality is another key foundation stone of the dairy sector that the Chinese government aims to improve. In June 2018 the State Council unveiled the dairy industry revitalization roadmap, prioritizing the establishment of premium milk source bases. Later in announcement No.1 [3] issued by the State Council this year, the development of dairy bases and improvement of infant formula product were mentioned again. All of these actions showcase China’s determination to revitalize its domestic infant formula industry and overhaul its whole industrial chain. In the next few years, infant formula revitalization will still be the theme of government’s work, and the competent authorities are expected to release more preferential policies, subsidies and incentive scheme to promote continued progress in China’s domestic sector.

2. Expedited infant formula registration approval

The former CFDA (now SAMR) released 34 batches of registered infant formula (amounting to 952 infant formula products) during the second half year of 2017. However, the approval rate dramatically slowed in 2018, and only 11 batches amounting to 243 formulas were announced in SAMR. Although the department restructuring and more stringent inspection standards were significant contributory factors in this delay, there is also no denying that delays in administration are also a significant contributor. During the two sessions (the National People's Congress and the Chinese Political Consultative Conference) of 2019, Hu Jiqiang, chairman of Conba, suggested that the competent authority should eliminate the work stoppage caused by institutional reform as soon as possible and follow the schedule stipulated in relevant regulations. Having received the proposal from the NPC member, the government will consider the optimization of infant formula registration approval procedure. Additionally, as China’s administrative institutions are almost universally undergoing extensive structural reforms we can expect optimization and streamlining of many processes.

During the two sessions (the National People's Congress and the Chinese Political Consultative Conference) of 2019, Hu Jiqiang, chairman of Conba, suggested that the competent authority should eliminate the work stoppage caused by institutional reform as soon as possible and follow the schedule stipulated in relevant regulations. Having received the proposal from the NPC member, the government will consider the optimization of infant formula registration approval procedure. Additionally, as China’s administrative institutions are almost universally undergoing extensive structural reforms we can expect optimization and streamlining of many processes.

3. Product traceability to bolster e-commerce safety

Online sales of infant formula has skyrocketed in China in recent years. The new CBEC policy issued at the end of 2018 and the reduction of CBEC comprehensive tax will further stimulate sales of infant formula on ecommerce platforms. However, optimism about investment prospects in this trade channel should be tempered by the realization that ecommerce enterprise and consumers still face potential safety risks such as fake products and false promotion. In August 2018, China unveiled the E-commerce law, which clarifies the responsibility of e-commerce operators and e-commerce platforms. As a high-risk food product, infant formula is given a high priority and product traceability is expected to be the focus of online supervision. According to cross-border e-commerce import retail announcement [4] jointly issued by 6 departments, China aims to establish the quality traceability system for products imported through the cross border ecommerce bonded warehouse model. The data should basically record all logistics info through the product chain of custody, such as the overseas consigner and manufacturers. Currently this traceability mechanism is piloted in some e-commerce platforms and bonded warehouses. For example, imported infant formula delivered from Ningbo bonded warehouse will be attached with a traceability QR code. It is predicted that this mechanism will be rolled out to customs across the nation. More significantly, the product traceability may become a mandatory requirement for infant formula enterprises who tend to access China through cross border e-commerce.

However, optimism about investment prospects in this trade channel should be tempered by the realization that ecommerce enterprise and consumers still face potential safety risks such as fake products and false promotion. In August 2018, China unveiled the E-commerce law, which clarifies the responsibility of e-commerce operators and e-commerce platforms. As a high-risk food product, infant formula is given a high priority and product traceability is expected to be the focus of online supervision. According to cross-border e-commerce import retail announcement [4] jointly issued by 6 departments, China aims to establish the quality traceability system for products imported through the cross border ecommerce bonded warehouse model. The data should basically record all logistics info through the product chain of custody, such as the overseas consigner and manufacturers. Currently this traceability mechanism is piloted in some e-commerce platforms and bonded warehouses. For example, imported infant formula delivered from Ningbo bonded warehouse will be attached with a traceability QR code. It is predicted that this mechanism will be rolled out to customs across the nation. More significantly, the product traceability may become a mandatory requirement for infant formula enterprises who tend to access China through cross border e-commerce.

4. Growth of organic

Dairy expert Song Liang said “The market size of organic milk powder (both online and offline sales) reached over 3 billion yuan in 2016, doubled in 2017, and is predicted to climb to over 10 billion yuan in 2018”. Obviously organic milk powder will be the next growth sector in infant formula industry, but these kind of products are subject to more stringent requirements in China. GB/T 19630.2-2011 stipulated that total concentration of organic ingredient should account for no less than 95% of the ingredients in the final products, therefore, the nutrient varieties that could be added into organic milk powder are very limited. Bound by these product formulation constraints, in terms of nutritional content, organic milk will not be able to compete with standard non-organic formula. Considering long-term industry development and consumer demand, ingredients that could be applied in infant formula may be given priority when it comes to organic certification, which would greatly benefit the organic milk powder industry. In June 2018, OPO was newly included in the 6th List of Certified Organic Products issued by China CNCA.

We provide full-scale global food market entry services (including product registration, ingredient review, regulatory consultation, customized training, market research, branding strategy). Please contact us to discuss how we can help you by

We provide full-scale global food market entry services (including product registration, ingredient review, regulatory consultation, customized training, market research, branding strategy). Please contact us to discuss how we can help you by