Request a Demo

Request a Demo

In 2019, overseas infant formula companies operating in China are facing increased stresses precipitated by a reduced birth rate, a decreased fertility rate in women, regulatory barriers and the continued upward trajectory of China’s domestic enterprise. Faced with these new challenges overseas enterprises are eagerly looking to find ways to offset emerging difficulties and improve their margins.

The standard cookie-cutter advice on offer is to align product development strategy to harness changes in consumer purchasing preference towards premium products and higher growth segments like organic and goats milk formula. Unfortunately, this standard advice has already occasioned a scramble to the top and has meant premium products and high-end niche segments will shortly become not so niche as evidenced by the high number of enterprises which have already launched or are in the process of developing premium products, goats milk, organic or A2 milk powder products. Although growth trends are promising, is launching premium, organic, goat milk or A2 IF enough to deal with the increased market pressures?

Assuming the answer is no, then what strategies are still available to international stakeholders to succeed in China’s IF sector? In this article, I will discuss methods to address current demand in China’s markets, and new strategies to align product development with the rapidly evolving demands of consumers in China’s baby care and infant nutrition sector. I will also touch on key “premium product” trends and will offer my thoughts and insights on the most important topics discussed during the Fourth China Special Food Conference [1], especially key points made by officials and senior dairy industry experts like Song Liang and Zhu Danpeng. For more general information about the IF market in China, challenges and solutions, you may check out ChemLinked’s recent report China Infant Formula Sector: 2019 Market Movement & Growth Strategy [2] for more info.

Low Birth Rate and Worrying Projections: Transitioning from “Quantity” to “Quality”

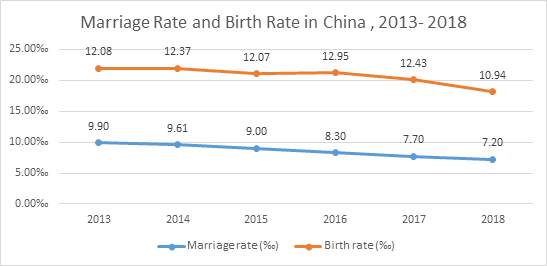

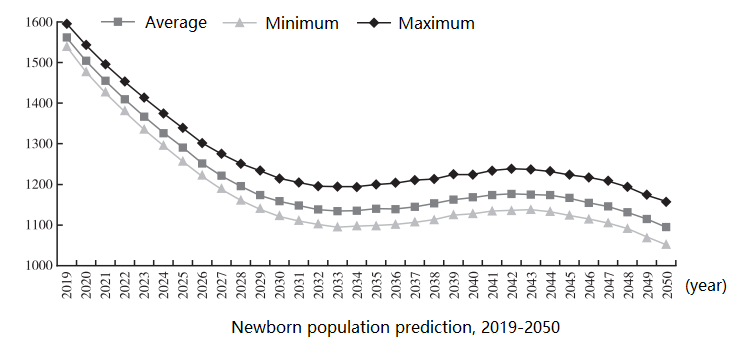

As the most basic factor dictating demand, China’s recent decline in birth rate has come as something of a surprise as it coincides with a massive change in social engineering policy by China’s government who recently ended its one-child policy. Expecting more births many companies had prepared to scale up production capacities but are now faced with a paradoxical reduction in the birth rate. Simply put fewer births equals fewer babies, less business and less to go around for international stakeholders operating in China’s infant formula sector. This decrease in birth rate has also been compounded by a decrease in marriage rates, as seismic shifts in China’s social structure play out in meaningful ways such as women placing increased emphasis on pursuing careers and putting off having children. Most projections predict that China’s birth rate will go through more corrections until it stabilizes and finds a new equilibrium at around 12 to 13 million newborns every year.

Source: National Bureau of Statistics of China [3]

Data from: Chinese Social Sciences Net, CSSN, July 23, 2019 [4]

Multiple other factors are shaping China’s infant formula market dynamics. The education level of women* has also drastically improved as to has their financial freedom. Inflationary pressures are also translating to increased living costs in China and many couples are now struggling to sort out mortgages and provide suitable accommodations for raising their children which is also another contributing factor to declining birth rates.

*Up to 2017, Chinese women took around 52% of graduates and 53% of postgraduates, Journal of Finance and Economics [5].

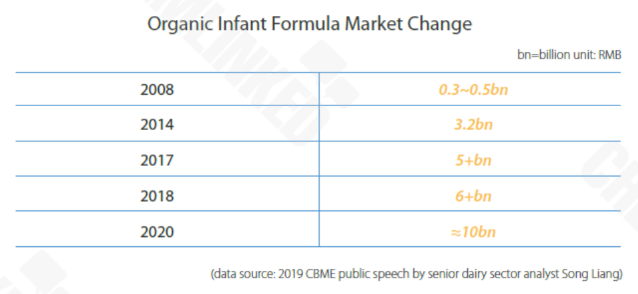

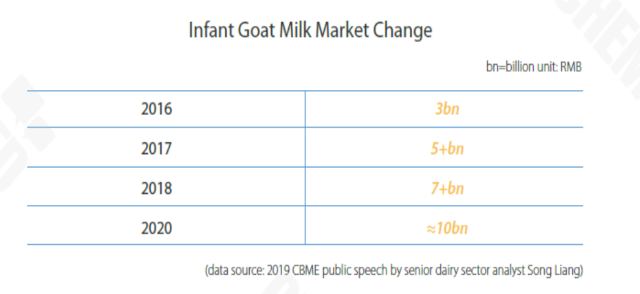

Based on this situation, senior dairy expert Song Liang believes, women who are willing to have children have the financial abilities to raise them well and they will spend more money to do so. Thus, although birth rates are trending downward, enterprises can still profit through product development strategies that focus on making ultra-premium products. Over the past several years we have seen a shift towards premiumization, but it is likely that many companies will need to go a step further in terms of investment in ingredients. Organic powder and goat infant formula have been performing extremely well. Beginning in 2017, both domestic and imported brands have focused on organic infant formula exemplified by product launches by Firmus, Beingmate, Ausnutria, Abbott, Nestle, Wyeth, Friso, etc. The number is still increasing. Until now, 267 goat infant formula have passed recipe registration and 51 organic products have been registered. Both sectors are expected to reach a valuation of 10 billion RMB annually by 2020.

Data: China Infant Formula Sector: 2019 Market Movement & Growth Strategy

We think the opportunities in these niche sectors are likely to be transient. As FOMU (fear of missing out) sets in and starts to dictate the product development strategies of dairy enterprise we envisage the almost inevitable situation where the market for both organic and goats milk trends towards saturation, and competition drives prices and margins down. The tight constraints on product development imposed by China’s infant formula national product standards, in the context of consumer purchasing and product development trends towards premiumization means it’s basically just a race to the top for all companies.

At Chemlinked we envisage an inevitable homogenization of product offerings in the premium segment. The number of permutations of premium optional ingredients, A2 protein, organic, goats’ milk, etc. is ultimately limited by the restrictions imposed by China’s GB 10765, and GB 10767 which list all the permitted ingredients that can be used in infant formula products in a positive list. With all other ingredients off the table, it's only a matter of time before the differences between products are essentially perceptional and created solely by the wizards in the marketing department of each company. Although the GB standards for infant formula are set to change, based on draft releases we don’t envisage any significant changes in ingredient scope. A HMO or two? Maybe? A tweak in the dosage or a change of a substance from optional to mandatory? Probably. But beyond this we envisage a situation where any innovation which drives profitability will be rapidly replicated by competitors in the market and rendered meaningless in short order.

It‘s important to remember that CBEC is an increasingly important retail channel for infant formula which also opens up avenues for unregistered organic and goats milk products which will also increase competition within the sector as awareness of the CBEC trade channel increases and as continued “opening up” reforms and trade facilitation measures are rolled out by China’s government

So, if the potential of organic and goats milk products eventually wanes or margins decrease, how can existing enterprise or new entrants to the market fight for a new business? The answer is to build a “consumer-oriented” sales model where enterprises prioritize brand building and building a closer relationship with consumers. In China brand recognition, engagement and trust are invaluable currency.

Building Stronger Relationships with Consumers

Time to focus on low-tier cities, combining online sales with offline promotion

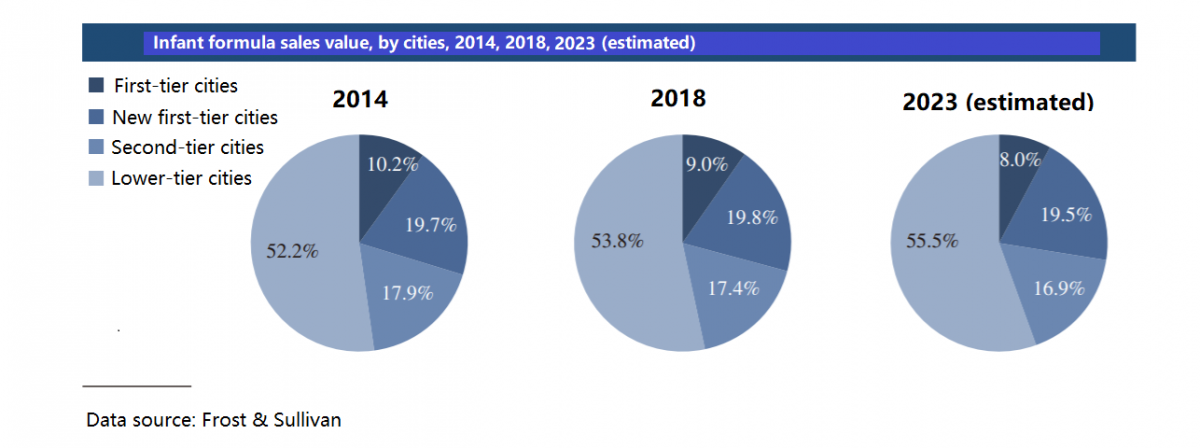

China is a large and complex market. According to different economic development speeds, cities in China can be divided into several tiers. Due to the high income, high purchasing power, and high e-commerce penetration, consumers in first and second-tier cities are often the first target of international stakeholders and thus these markets are generally mature and characterized by fierce competition. Lower birth rates in the context of an already mature market have meant that the markets in first and second-tier cities are reaching or have reached saturation point. Many enterprises have already noticed this change. Consumers in low-tier cities are the next target. According to predictions made by Frost & Sullivan, the infant formula sales value in lower-tier cities will account for 55.5% of all sales by 2023. According to Enda Ryan [6], CEO of Mead Johnson Nutrition Greater China, in 2017, there was 4.5 million infants (from 0~3 years old) in first-tier cities, 5.4 million in second-tier cities and 38 million in the rest of China. A large population of newborns means a large potential market. But do consumers in these low-tier cities possess strong enough purchasing power? Do premium products have a place in these markets or do product development strategies have to be tweaked to align with consumer demand there?

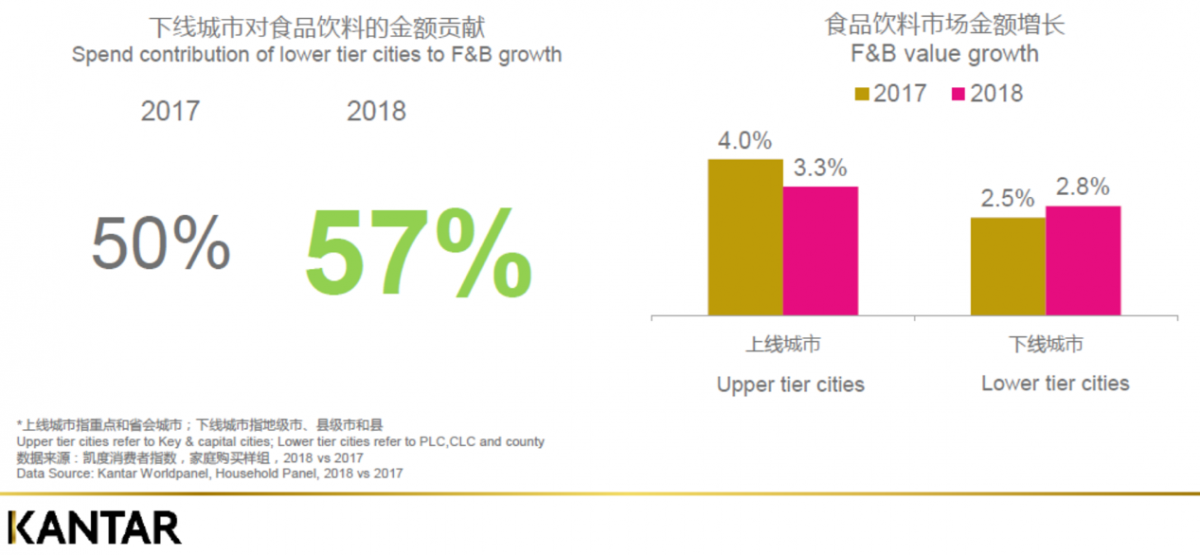

Lower birth rates in the context of an already mature market have meant that the markets in first and second-tier cities are reaching or have reached saturation point. Many enterprises have already noticed this change. Consumers in low-tier cities are the next target. According to predictions made by Frost & Sullivan, the infant formula sales value in lower-tier cities will account for 55.5% of all sales by 2023. According to Enda Ryan [6], CEO of Mead Johnson Nutrition Greater China, in 2017, there was 4.5 million infants (from 0~3 years old) in first-tier cities, 5.4 million in second-tier cities and 38 million in the rest of China. A large population of newborns means a large potential market. But do consumers in these low-tier cities possess strong enough purchasing power? Do premium products have a place in these markets or do product development strategies have to be tweaked to align with consumer demand there? According to data from Kantar[7], the FMCG sector in China grew by 5.2% in 2018, mainly driven by China’s consumption upgrade and urbanization. Lower-tier cities contribute more to overall growth as shown below. Other data shows that the quantity of young families (referring to people aged from 20 to 35 years old) in lower-tier cities makes up 68% of this demographic in China and happens to represent the key target consumer group for infant formula companies.

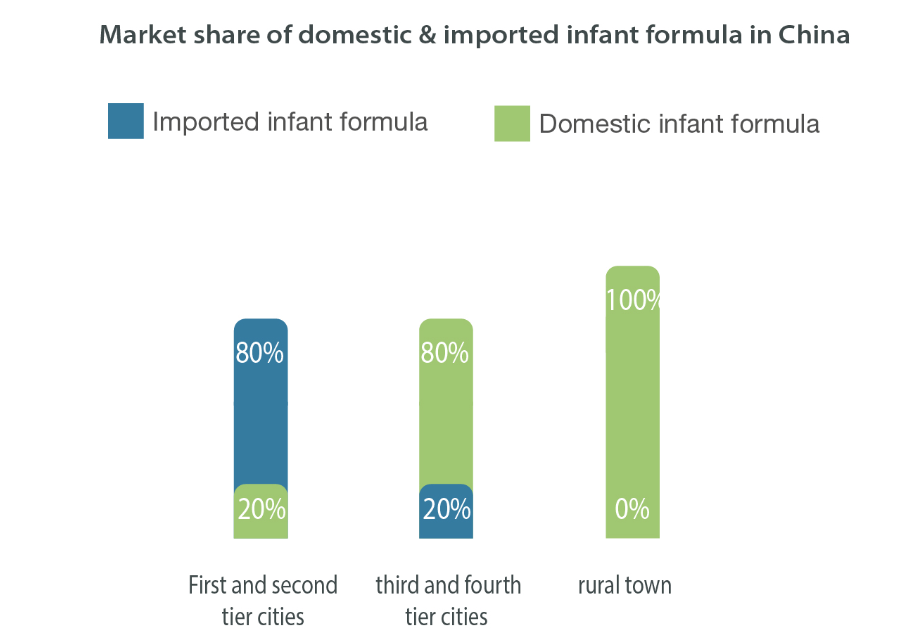

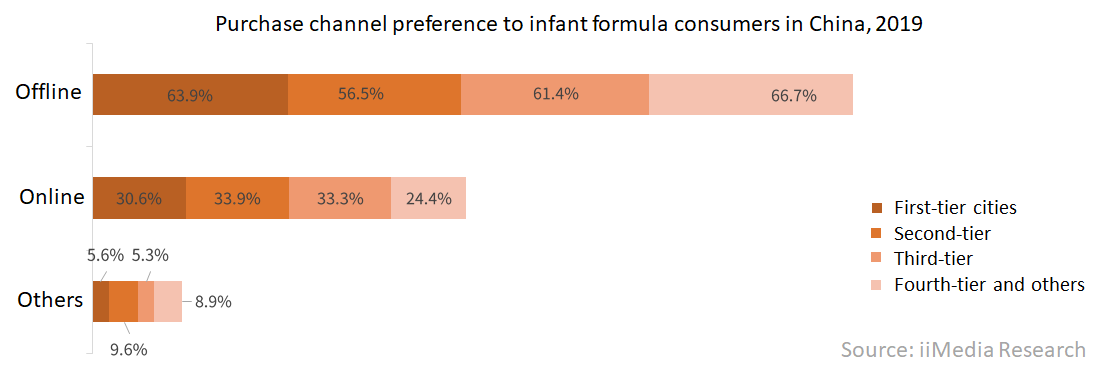

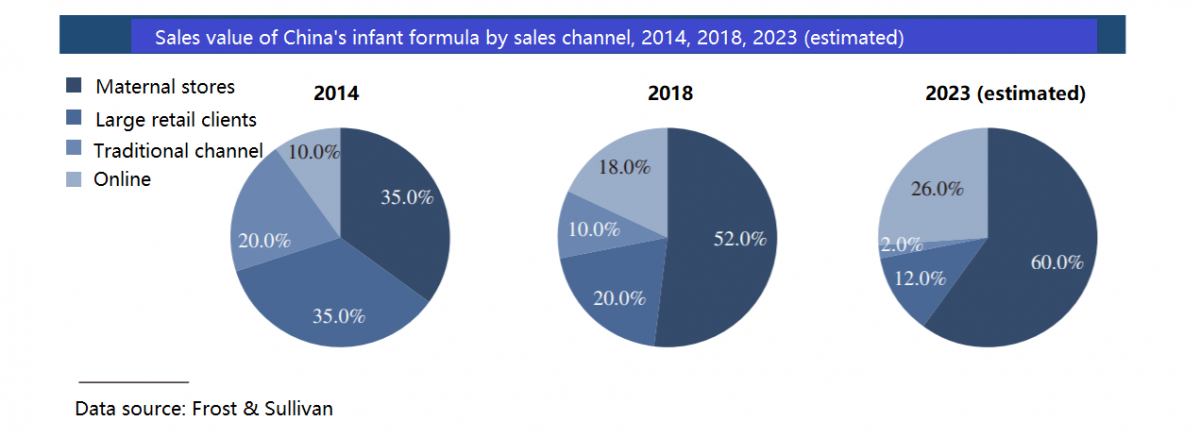

According to data from Kantar[7], the FMCG sector in China grew by 5.2% in 2018, mainly driven by China’s consumption upgrade and urbanization. Lower-tier cities contribute more to overall growth as shown below. Other data shows that the quantity of young families (referring to people aged from 20 to 35 years old) in lower-tier cities makes up 68% of this demographic in China and happens to represent the key target consumer group for infant formula companies. Although there is huge potential in low-tier cities, it is hard for international stakeholders to compete with local brands. According to China Import & Market Data of Major Food Sectors 2018 [8], imported infant formula only occupies 20% of these markets. Why? The difference lies in the sales channel. Consumers in third and fourth-tier cities, prefer to use offline channels to purchase infant formula, especially maternal stores. According to Frost & Sullivan, the maternal store channel will account for 60% of infant formula sales in 2023. Targeting low-tier cities is a huge factor in the rapid ascension of Chinese owned brands Firmus and Ausnutria in the last several years.

Although there is huge potential in low-tier cities, it is hard for international stakeholders to compete with local brands. According to China Import & Market Data of Major Food Sectors 2018 [8], imported infant formula only occupies 20% of these markets. Why? The difference lies in the sales channel. Consumers in third and fourth-tier cities, prefer to use offline channels to purchase infant formula, especially maternal stores. According to Frost & Sullivan, the maternal store channel will account for 60% of infant formula sales in 2023. Targeting low-tier cities is a huge factor in the rapid ascension of Chinese owned brands Firmus and Ausnutria in the last several years.

Why does offline promotion matter?

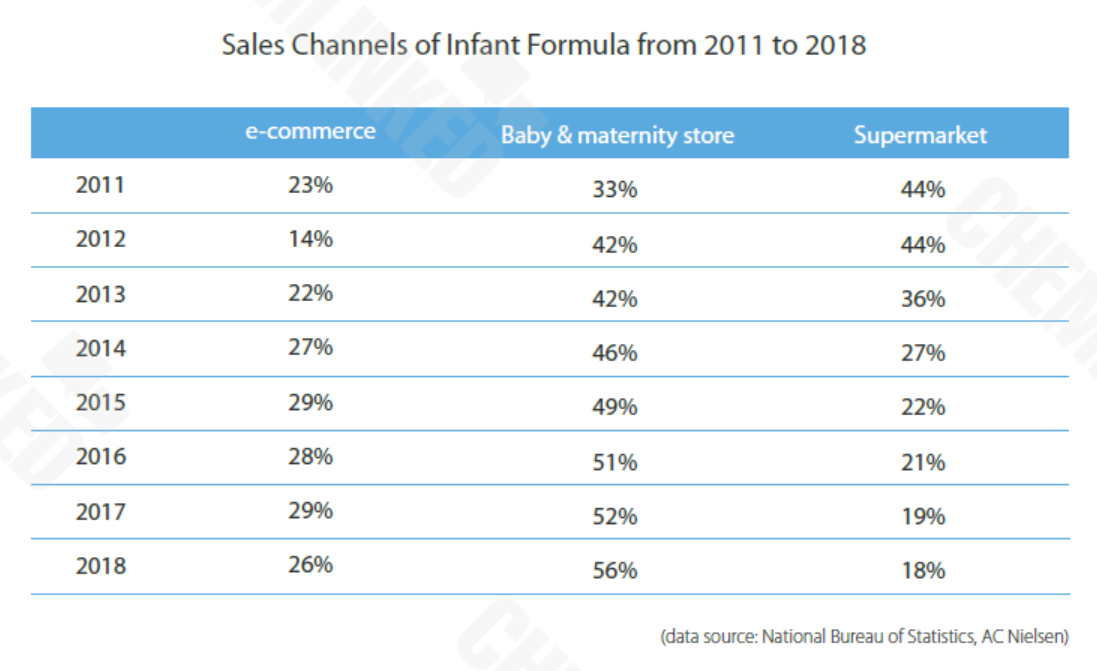

Compared to traditional maternal stores, e-commerce platforms offer better margins and ultimately translate to better deals for consumers. Consumers also benefit from the convenience and freedom to choose and order the products they want. The proportion of the market value attributable to e-commerce has been steadily rising as well. However, if you take an overall analysis of the sales value of different retail channels, you will find e-commerce growth pales in comparison to maternal stores. (data from Nielsen)

Data: China Infant Formula Sector: 2019 Market Movement & Growth Strategy

Offline promotion is still crucially important. Moreover, solid offline promotion can also attribute to an increase in online sales. We advise enterprises to invest heavily in combining the promotion of offline and online sales and learn from the success of Firmus which invested heavily in both online and offline promotion with the result of realizing major growth through both channels.

A case study of Firmus: How to serve and educate consumers and build multichannel brand recognition?

According to Firmus’s IPO document [9] released this year, from 2016 to 2018, Firmus’s revenue reached 3.18 billion RMB (2016), 5.416 billion RMB (2017), and 9.199 billion RMB (2018), driven by an average YOY growth rate of 70%. On the first page of its IPO document, Firmus emphasized the importance of the maternal store channel. From 2016 to 2019, the number of its distributors and retailers was 58k (2016), 67k (2017), 90k (2018) and 109k (2019). In order to better manage its retailers Firmus also set up an independent customer service department to manage the traffic coming from its major retailer stores (especially the one with excellent sales performance).

*Feihe successfully listed on the Hong Kong Stock Exchange on November 13, 2019. View the news at ChemLinked China Dairy Giant Feihe Lists on Hong Kong Stock Exchange.

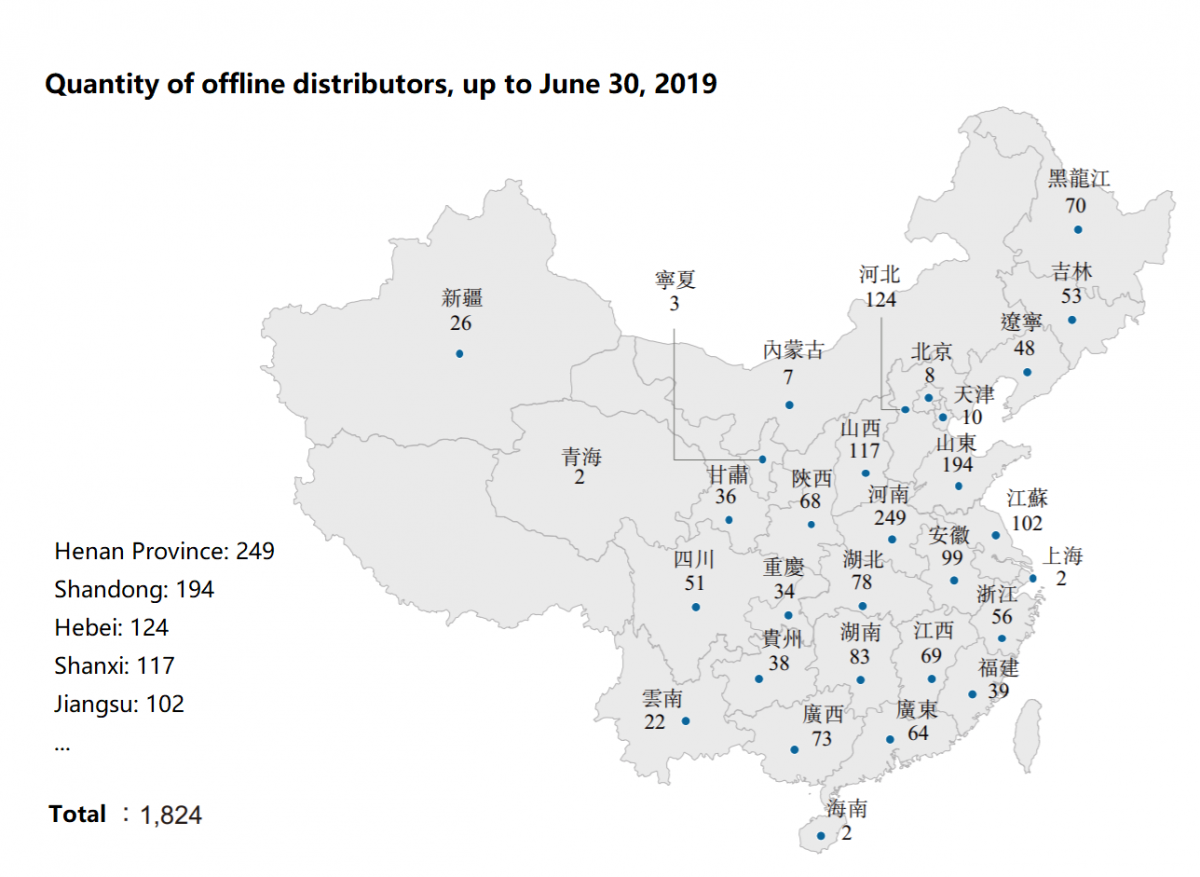

Firmus had over 1800 distributors in China up to June 30, 2019. To put things into perspective, Beingmate, once the dominant player in low-tier cities was once renowned for its strong distribution channels. At its peak, Beingmate had 1000 distributors. Firmus has now 1800 distributors and counting, almost twice that of Beingmate. ( In 2015, Beingmate underwent major company restructuring and culled the number of distributors down to just 500 distributors [10])

Source: Firmus’s IPO document

Firmus adopts a multi-channel marketing and retail strategy allowing it to target a wider scope of consumers and holds over 300 thousand offline face-to-face seminars a year. Firmus also offers a lot of engaging services on social media, social e-commerce, Wechat and also more traditional media forms like TV, radio broadcasts and newspapers. This multipronged approach has allowed it to gain significant traction amongst Chinese consumers and build strong brand recognition. Firmus also plays up its home-field advantage by leveraging the concept that it is an infant formula “developed to be more suitable for Chinese babies”.

Combining online sales with offline promotion to promote CBEC

Up to now, China has approved 1269 infant formula recipes (view the full list at ChemLinked F-list [11]), covering almost all the mainstream and demanded brands. Going forward China will also be stricter with recipe registration and will slow the rate of onsite inspection approval to control the quality and quantity of infant formula on the market. In June 2019, China consulted on the Infant Formula Recipe Registration Measures [12] to raise more requirements for onsite inspection. Increased regulation only further emphasizes the advantages of CBEC as a viable trade channel in China, particularly for infant formula stakeholders that haven’t registered their product.

However, we must look at the potential of CBEC in the context of market dynamics particularly the fact that:

The market in first and second-tier cities is already saturated meaning low-tier cities is the only battleground which offers obvious potential

Consumers in low-tier cities do not generally use e-commerce to purchase infant formula

Consumers in lower tier cities choose domestic products 80% of the time

According to Ali Research, CBEC sales in low tier cities on Tmall global didn’t increase fast in 2017

Based on these facts is CBEC really a viable route to market for companies? According to Song Liang, in the future, offline promotion of online CBEC retails channels will start to play a more important role, which will hopefully improve CBEC sales in third tier and fourth-tier cities.![]()

Source: Deloitte report [13]

Product Development and Market Strategies: Localization, Digital Assets, Multichannel Marketing, New Retail and Everything in Between

There is no single factor that can guarantee success in China’s infant formula sector. Rather it is necessary to implement a multipronged strategy that addresses rapidly evolving changes in consumer purchasing preference and leverages key digital assets in both retail and marketing.

Consumer engagement is crucial, and consumers are increasingly expecting services that go far beyond the delivery of a top-quality and safe products made using the finest ingredients. Today Chinese consumers are expecting excellent customer service and educational content delivered over easily accessible platforms like Wechat or delivered from trustworthy sources. They are also expecting better value for their money and being rewarded for their loyalty. Harnessing digital word of mouth has also become vital in ensuring traction with Chinese consumers evidenced by the rapid rise of social e-commerce platforms like Red, Wechat and group purchasing like Pinduoduo.

Beyond all this consumers are expecting enterprises to enrich their lives and improve the prospects of their family and most importantly their children. Content channels promoting non-biased medical information, nutritional information, dietary and meal planning advice, baby care etc. are all becoming key battlegrounds for the marketing departments of infant formula companies. As pointed out by the expert, Song Liang, building a successful brand isn’t achieved by simple cooperation with pop stars or KOLs but must be achieved by consumer recognition of your brand, trust and engagement.

Food for Thought: Leveraging the concept of generational care

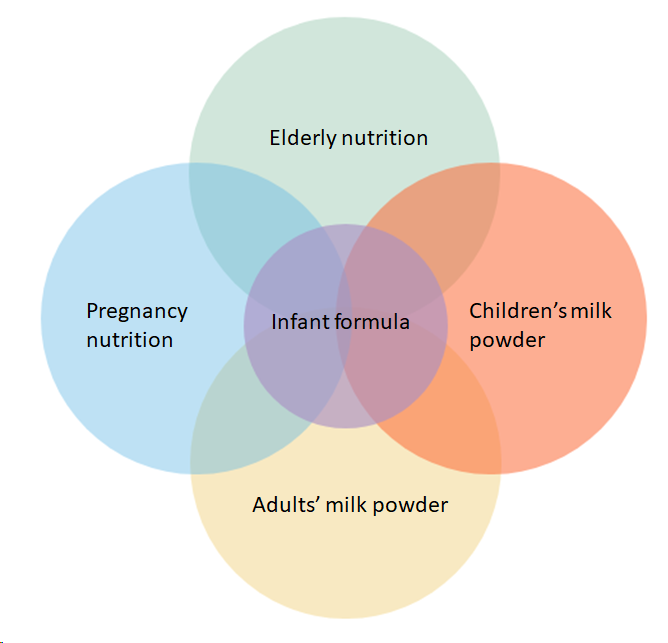

Infant formula enterprises must expand their product portfolios, design products for the whole family and leverage the concept of generational care, with infant formula brands as the cornerstone of the strategy. The concept of family generational care in product development addresses the various stages of life for each family member to ensure health, wellness and optimal quality of life.

Consumers who have chosen the infant formula of a specific brand for their babies, already have loyalty and trust for that brand and the product quality.Mums are unlikely to switch products once they are happy with one an as the family’s chief shopper are more likely to buy other nutritious products for their family members and more likely to trust a brand which they use on their baby. Building “lifecycle management” and generational care into product offerings will be another great tactic to build brand recognition and leverage less saturated markets with great growth potential. Besides liquid milk, companies can also provide nutritional products such as children’s milk powder when the babies grow up, adult milk powder for parents and also aged nutrition for the elderly. Nutritional products targeting specific demands such as products for pregnant women and also food for special medical purposes are good options.

Actually, some companies have already begun to do this strategy. However, this topic is however beyond the scope of this article and will be covered in my next article. Stay tuned for more info.

Actually, some companies have already begun to do this strategy. However, this topic is however beyond the scope of this article and will be covered in my next article. Stay tuned for more info.

We provide full-scale global food market entry services (including product registration, ingredient review, regulatory consultation, customized training, market research, branding strategy). Please contact us to discuss how we can help you by

We provide full-scale global food market entry services (including product registration, ingredient review, regulatory consultation, customized training, market research, branding strategy). Please contact us to discuss how we can help you by