Request a Demo

Request a Demo

In the few years, baby product sector in China experienced an outstanding market diversification, product differentiation and expansion of customer base. The most important consumers are the generations born after 1980 and 1990, and this is why manufacturers and sellers, apart from fulfilling safety and health needs, need to develop successful strategies to attract them. As a consequence of changes to China’s 1 child policy, baby nutrition is the fastest growing sector in this market, offering brilliant future investment potential. However, we can no longer rely only on organic products and new brand names to drive this growth; we should focus more on product concept innovation and upgrading the customer base. Before we do so we should first get acquainted with some contemporary trends and this is why some of the data presented by CBN Data in their “Big Data Report on Online Baby Nutrition Consumption Trends” is so rel evant for us.

Domestic or foreign?

Baby food market is dominated by infant formula. Population growth and low breast feeding rates are the main triggers of the expansion in this sector. There are many different domestic brands, but imported produce still holds the biggest share of the market. CBN reports that in online sales, foreign products surpass domestic ones by about 50% and their total market share in 2015 was 60%. Market concentration is very high, with 10 brands leading. With regard to other child nutrition categories, it is noteworthy to mention that in recent years more and more customers are choosing Chinese products over imported ones; this tendency is particularly conspicuous among the youngest demographic of the analyzed sample. In fact, parents born in the 90s seem to make more traditional choices, as Chinese products account for a 40,92% of their chosen options, but is just 25.63% for 80s generations, despite the fact that the first group had a closer and more prolonged contact with foreign goods. Also significant is the fondness of 90s generations for food products enriched with eyesight and brain capacity enhancing products. Apart from staple and nutritious food, we should also keep an eye on baby snacks, a market whose rise we shouldn’t underestimate. In this subcategory, nori seaweed is the product showing the highest growth, closely followed by milk tablets, Puffs, Fruit bars and sausages.

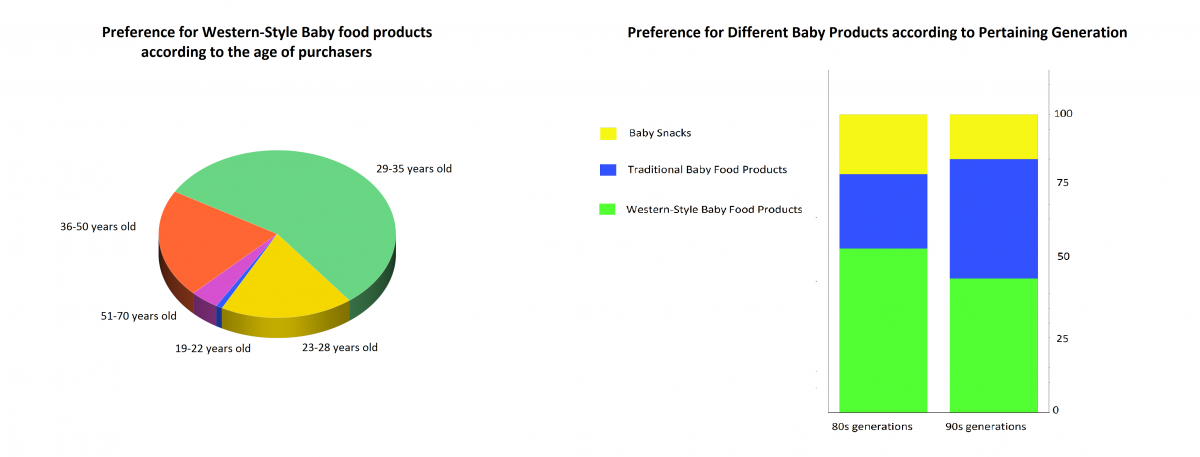

Age difference

A commonly accepted way of distinguishing between different age spans is 1-4 years old, 4-6 years old and 6-12 years old; babies’ needs change according to their stage of life.1-4 years old children are still beginning to learn to walk and talk and according to CBN Data Report the most popular products for this category are bone growth fortified foods. The fastest rising products for this age span are natural lungs tonic and honey, showing a 47,7% growth rate. For 4-6 years old children, excluding bone growth supplement enhanced food, vitamin and mineral enhanced food are the fastest growing products and for the last category, 6 to 12, except for vitamin and mineral fortified items, we should look with attention at immune system strengthened foodstuffs. Talking about gender, it is no surprise that women dominate the market, as 70% of total expenditure comes from their pocket, but in differentiating market sectors the age of parents is also important: the ones born in the 1980s are the leading buy force, with 29 to 35 years old occupying a market share of 46.59%, compared to 23-28 years old occupying a 20.16%. However, 90s generations spending capacity is the one increasing more, rising from 25.10% of the total in 2015 to this years’28.59%.

Geographic Differences

CBN Data report also shows that the way mommies and daddies nurture their beloved babies changes according to where they live. Parents in western China are most interested in western products, with Xinjiang mothers manifesting this tendency in the strongest way and Sichuan ones following closely. The difference in the domestic product purchasing preference is not that relevant but it’s interesting to notice that consumers in International cities like Shanghai and Beijing are the least likely to purchase domestic products, with Shanghai leading this group. Even though the basis of this market is still fragile, Shanghai babies are the ones who eat healthy snacks the most, while North East and Inner Mongolia are the biggest consumers of milk tablets and other milk based products. It is also interesting to know that many northwestern parents are nouveau riches and they are willing to buy very pricey children supplements: Gansu ranks second in the top ten of the propensity to spend, and Xinjiang third.

Part two: Purchasing Channels of baby products market

Talking about the current situation of the infant nutrition market in China, the keywords that come to us in mind are product innovation-upgrade and channel differentiation. This market has much better development possibilities than before, but in order to grasp customers’ needs an understanding of the pros and cons of different sales channels is important. Different channels require distinct strategies, like optimizing the offer by dividing baby product customers in groups, improving online shops’ price management systems, optimize product differentiation etc. This is why some of the data in Nielsen’s “Blue Book on the Baby Product Industry of China” are particularly significant.

Online vs Offline: Who will win the battle?

Analyzing both online and conventional shops customers, the report discovered that online shops purchasing is preferred mainly for being more convenient, while physical stores are generally chosen for their professionalism and safety. In online purchases, customers are very attracted to features like “save time”,“door to door”,“easy to compare”,“24/24 order”, while in physical stores the quality of goods and the shopping experience are the most important things they consider. In addition, even though the habitual customers of overseas online shops represent a relatively low percentage (5%) of the total, they belong to the highest salary and education group and generally look for high quality, certified and/or high price products. Under the impact of imported online purchases, the frequency and spending capacity of physical shop customers is decreasing. Based on this we can assume that foreign goods sales will still increase. However, given the uncertainty of future policies the extent of this growth cannot be foreseen.

Ongoing trends and advice

Since 2003 to the 3rd quarter of 2016, offline price of baby formula experienced an average annual growth of 11%, and this tendency didn’t decelerate with the slowdown of GDP growth. One of the drivers of price rise is the premiumization of the sector, a trend that started along with the increase in imported original packaging and organic baby formula. Adapting to this trend, many manufacturers began their own process of premiumization including medication of formula, use of more expensive ingredients like OPO, GOS, FOS, ARA, DHA, EPA etc. Offline purchases also deserve attention by retailers and producers, first of all because mother and baby shops in lower level cities and villages still occupy a significant percentage of the total and secondly, because urban purchasing of baby products is scattered. The influence of the registration system of baby formula also constitutes a good business opportunity.

One of the new trends under way is the development of integrated retail channels which combine elements of both online and offline retail. Some products that were previously only available online or offline are now ubiquitous and consumers now have a wider range of purchasing channels. Secondly, consumer dependency on online retailers’ stock promotions increased (on an average, the participation in such activities increased 5% compared with the same period in the previous year). Producers lowered prices to increase sales generating a fierce and counterproductive price war that negatively impacted the majority of retailers. In this challenging environment, apart from managing prices, producers should also pursue product differentiation and organize online promotion activities and other similar actions to increase sales.

Part three: Main Regulations for Baby Food Products

All food products produced and sold in China should comply with China’s Food Safety Law, and should respect requirements on food additives, as well as the ones regarding food contact materials and food labeling regulations. The standard for nutrient fortification substances is instead GB 14880, which regulates the nutrients allowed to be used. In these regards, baby products are no exception. However, Imported Infant formula is also subject to a special legal framework, we invite you to take a look at it.

As for the other baby food products, a lot of them fall into the category of Food for Special Dietary Purposes, and are also subject to the following GB standards (among others):

- Q&A of GB 13432-2013 Labeling of Prepackaged Foods for Special Dietary Use ;

- Administrative Measures for Registration of Foods for Special Medical Purpose ;

- GB 22570-2014 National Food Safety Standard Complementary Food Supplements ;

- GB 31601-2015 National Food Safety Standard Nutrient Supplementary Food for Pregnant and Lactating Women ;

- GB 10770-2010 National Food Safety Standard Canned Complementary Foods for Infants and Young Children ;

- GB 13432-2013 National Food Safety Standard Labeling of Prepackaged Foods for Special Dietary Uses ;

- GB 10769-2010 National Food Safety Standard Cereal-based Complementary Foods for Infants and Young Children ;

Others fall into the category of Food for Special Medical purposes, while some of them are filed under Health Foods. Last but not least, all regulations on baby products are subject to constant change and this is why we invite you to always be updated. Here are some recent news you can find on our website:

- New Testing Items for China Infant Formula Sampling Inspection -China to Start the Revision of Infant Formula National Standards ;

- China to Start the Revision of Infant Formula National Standards ;

- China Infant Formula: CFDA Finalized Labeling Requirements for Infant Formula Recipe Registration ;

- China Infant Formula: New Regulations Reshaping Market Landscape.

Perspectives of growth are brilliant, but entering this market will be harder in the future, don’t wait too long!

Companies mentioned in the article:

CBN Data is China's largest and most comprehensive financial media group. Founded in Shanghai in 1993, it is specialized in news, advertising, marketing, financial and investment consulting, reports and financial data services.

Nielsen is a global information, data, and measurement company headquartered in the United States. It operates in over 100 countries (China included) and employs approximately 44,000 people worldwide.

We provide full-scale global food market entry services (including product registration, ingredient review, regulatory consultation, customized training, market research, branding strategy). Please contact us to discuss how we can help you by

We provide full-scale global food market entry services (including product registration, ingredient review, regulatory consultation, customized training, market research, branding strategy). Please contact us to discuss how we can help you by